迈瑞医疗再加仓:在估值底部,与内部人的“真金白银”站在一起

Adding to My Mindray Position: Siding with Insiders’ “Real Money” at Rock-Bottom Valuations

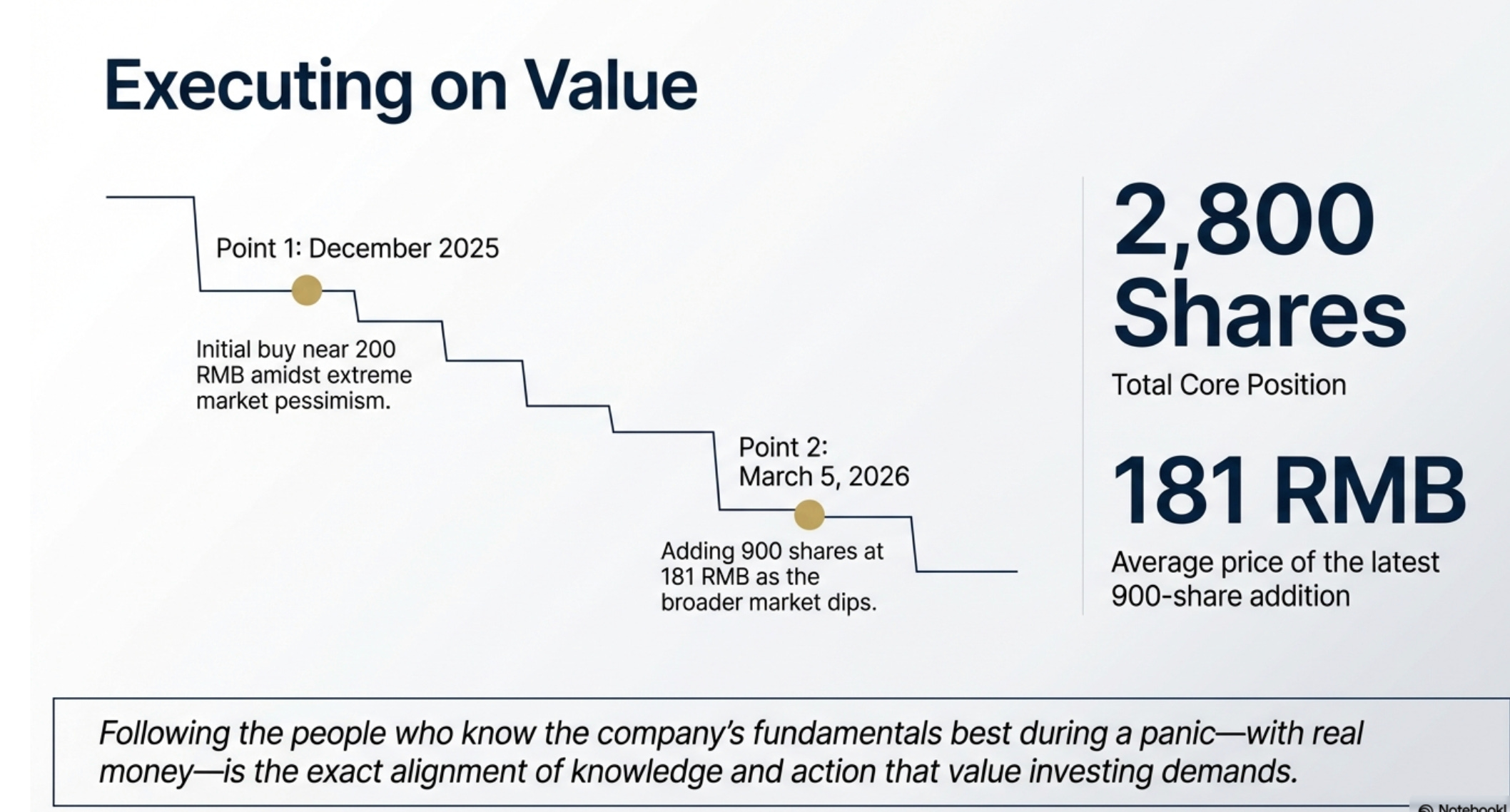

今天,我以 181 元的均价再次加仓 900 股迈瑞医疗(SZ:300760),目前总底仓累计达到 2800 股。

Today, I added another 900 shares of Mindray Medical (SZ:300760) at an average price of 181 RMB, bringing my core holding to a total of 2,800 shares.

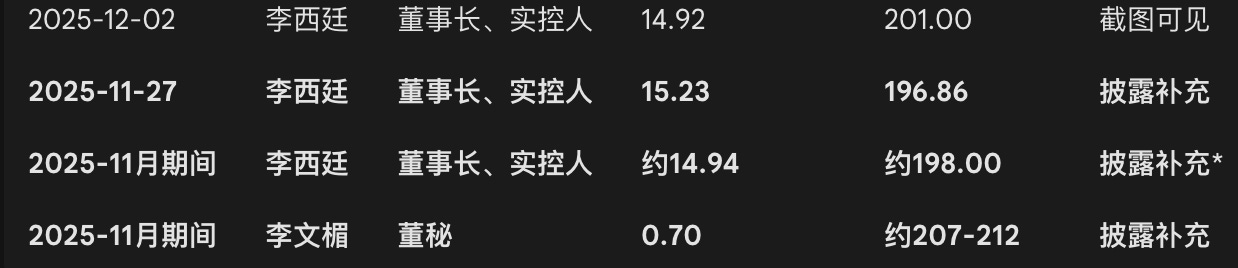

去年 12 月,在市场情绪极度悲观时,我选择相信大股东李西廷 2 亿元的“闪电”护盘,在 200 元附近建仓。而今天,当股价随着大市进一步下探至 180 元区间时,高管李朝阳等人的接力增持再次亮明了内部人士(Insider)的底牌:目前的估值已经跌出了深厚的安全边际。在恐慌中跟随最了解公司基本面的人买入,是价值投资中必须践行的知行合一。

Last December, amidst extreme market pessimism, I chose to trust the 200-million-RMB “lightning” defense by the controlling shareholder, Li Xiting, and initiated my position around the 200 RMB mark. Today, as the stock price tracked the broader market down to the 180 RMB range, the relay buying from executives like Li Zhaoyang once again revealed the insiders’ hand: the current valuation has fallen into a deep margin of safety. Following the people who know the company’s fundamentals best during a panic—with real money—is the exact alignment of knowledge and action that value investing demands.

支撑我越跌越买的底层逻辑,始终是那条第一优先级的筛选标准:商业模式的质量。

The underlying logic supporting my decision to buy the dip remains my absolute first-priority screening criteria: the quality of the business model.

市场往往容易被短期的宏观情绪或单一的设备招标降价新闻所干扰。但如果穿透到真实的临床科室运营层面,无论是高端医学影像、重症监护系统,还是 IVD(体外诊断)流水线,其真正的护城河从来不仅仅是纸面上的技术参数,而是极高的科室粘性、深度的医生工作流绑定以及极其昂贵的系统替换成本。

The market is often distracted by short-term macroeconomic sentiments or noise surrounding centralized procurement price cuts for single devices. However, if we look through to the actual operational level of clinical departments—whether it’s high-end medical imaging, critical care monitoring systems, or the IVD (In Vitro Diagnostics) pipeline—the true moat is never just technical specs on paper. It lies in extreme department stickiness, deep integration into doctors’ workflows, and exceedingly high system replacement costs.

迈瑞正在完成一场从“卖设备”向“卖流水”的底层商业模式蜕变。目前其国内业务中,以 IVD 试剂为代表的流水型耗材业务占比已突破 60%。这种经典的“设备+试剂”剃须刀模式,叠加近期与艾迪康(ICL)、IHH 医疗集团等海内外巨头的密集结盟,直接锁定了未来的高频复购和抗周期的稳定现金流。

Mindray is completing a fundamental business model transformation from “selling equipment” to “selling recurring revenue.” Currently, in its domestic business, the recurring consumable business represented by IVD reagents has exceeded 60% of total revenue. This classic “razor-and-blades” model, coupled with recent intensive strategic alliances with domestic and international giants like ADICON (ICL) and the IHH Healthcare Group, directly locks in future high-frequency repurchases and counter-cyclical, stable cash flows.

在估值层面,我运用查理·芒格常用的“预期投资法”(反向DCF模型)进行推演:按照保守的常态化 110 亿自由现金流基数和 9% 的折现率计算,当前 181 元的股价,意味着市场仅仅计入了其未来区区 5% 的极低年化增速预期。而如果按其合理的 10% 增长测算,绝对内在价值应在 266 元附近。对于一家流水型业务过半的高端医疗龙头,这完全是将其视作“公用事业股”的错杀定价,恰恰为我们砸出了极其宽阔的安全边际。

On the valuation front, applying Charlie Munger’s favored “Expectations Investing” approach (Reverse DCF): based on a conservative normalized free cash flow base of 11 billion RMB and a 9% discount rate, the current 181 RMB stock price implies that the market is pricing in a dismal annualized growth expectation of merely 5%. If calculated at a reasonable 10% growth rate, the absolute intrinsic value sits around 266 RMB. For a high-end medical leader with over half its revenue coming from recurring streams, this mispricing treats it like a stagnant “utility stock,” which is exactly what creates our incredibly wide margin of safety.

在 A 股缺乏期权工具进行风险缓冲的现实下,左侧做多优质资产完全依靠对企业内在价值的笃定(基本面确认:这是我愿意持有 5-10 年的公司吗?)。今年初以来,上百家海外长线机构的密集调研已经释放了资金重新定价的信号。在 3 月 31 日年报最终交卷前,用 181 元的筹码夯实这 2800 股底仓,买入的不仅是静态的低估值,更是其在全球高端医疗市场持续攻城略地的确定性。

Given the reality that the A-share market lacks options tools to buffer risks, going long on high-quality assets on the left side relies entirely on a deep conviction in the enterprise’s intrinsic value (Fundamental check: Is this a company I am willing to hold for 5-10 years?). Since the beginning of 2026, intensive research visits by over a hundred foreign long-term institutional investors have signaled a repricing by smart money. Before the final annual report is delivered on March 31st, using chips at 181 RMB to solidify this 2,800-share core position is not just buying a statically low valuation; it is buying the certainty of Mindray’s continued market share expansion in the global high-end medical market.